|

Getting your Trinity Audio player ready...

|

In the face of global economic uncertainty and widespread political upheaval, what lies in store for the art and finance industry in 2024? According to the latest Deloitte Private and ArtTactic Art & Finance Report, we could be in for a period of intense adaptation and diversification, with the importance of art in wealth management only rising and ultra-high-net-worth individuals (UHNWIs) linking more of their wealth to art and collectibles.

Using insights gleaned from a survey of 435 industry stakeholders and contributions from 55 experts, the report paints a nuanced picture of an industry grappling with the challenges of transparency and regulatory modernization. Yet, it also shows a sector that is resilient, adaptable, and poised to benefit from a shift towards holistic wealth management.

At the same time, the report highlights the art market’s sluggish growth, primarily due to its concentration at the top end and the lack of transparency affecting trust and efficiency. Significant shifts are also noted in the demographic profile of art collectors and investors, with younger generations and Asian buyers becoming increasingly prominent. This change is accompanied by a growing interest in sustainable and socially responsible investments, particularly among younger collectors.

Jing Daily Culture recently caught up with report co-authors Anders Petterson of ArtTactic and Adriano Picinati di Torcello of Deloitte to discuss the findings of their new report, with the pair delving into the reasons behind the art market’s sluggish growth, the impact of luxury collectible sales on the traditional art market, the changing demographic of art collectors, and much more.

What are some of the factors that contributed to the sluggish annual growth rate of the art market compared to the overall wealth increase among UHNWIs?

The art market’s strong concentration toward the top end is both a blessing and a curse. This might explain the anemic growth of the art market over the last 10 years. We are currently facing a scenario where a few artists’ markets are accumulating disproportionately large amounts of the wealth generated in today’s art market, leaving a relatively small share for 99% of the remaining artists. So, if we want the art market to grow and direct more wealth toward supporting artists, we need to look at the inherent inequality that exists in the art market today, and see how wealth could be more evenly distributed to build a stronger and more sustainable art sector.

The challenges facing the art market remain relatively unchanged over the last decade and could be a reason for stagnated sales growth over the last 14 years. While the art market often shrouds itself in confidentiality, there is a fine balance between confidentiality and mistrust. Lack of price and transaction transparency often leads to asymmetric information availability between actors in the art market and can undermine trust.

Can the art world continue to resist consumers’ demands for more transparency through reliable and instantly accessible information? In a world where misinformation is an ever-increasing problem, it is critical for confidentiality and transparency to coexist in the art industry. This requires a new framework; new technologies (like blockchain) and new data ownership and access models could support both confidentiality where it is required while providing the right level of transparency to create a more efficient and trusted marketplace.

Challenges remain in integrating art into wealth management. Image: Shutterstock

How does the surge in luxury collectible sales impact the traditional art market, and what synergies can be leveraged?

Luxury collectible sales reach new heights in 2022 and could signal new opportunities for the art and finance industry: The growth potential of the luxury collectibles market is evident by its auction sales surge over the last two years, reaching a record high in 2022.

We expect to see a growing interest in the financialization of luxury collectibles and the potential to tap into the much broader and larger US$1.5 trillion luxury goods industry. This will also have implications for stakeholders in the luxury market that should also start integrating this financialization into their business strategy.

Has there been a change in the demographic profile of art collectors and investors over the past decade?

These findings are based on research from ‘Sotheby’s and ArtTactic Peak Performance Report: The market beyond $1m 2018-2022’ which was quoted/ mentioned in the Art & Finance Report 2023. This report shows that in the last 5 years we see a demographic shift from older buyers (baby boomers) to younger generations of buyers (GenX and Millenials), and an increasing presence of Asian buyers, making up nearly a third (32%) of those who placed bids for $1m+ art at Sotheby’s between 2018 and 2022.

More younger buyers are entering the top-tier market. Although the “Baby Boomer” generation was still the largest group (40.6%) of bidders in the $1m+ market in 2022, the number of them is down from 48% in 2018. Meanwhile, Millennial bidders (born 1981–96), have increased from 7% in 2018 to 16% in 2022.

NextGen collectors have different needs and preferences. NextGen collectors drive digital transformation: 80% of young collectors believe in blockchain as an asset register for art and collectibles, and 79% see the rapid developments around artwork identification technologies as instruments to address many of the current inefficiencies in today’s art market.

Younger collectors more open to new art investment models. The interest in fractional ownership among the younger collectors surveyed is significantly higher this year than that of older collectors, with 50% (up from 43% in 2021) saying that they are interested in these types of investment. Young collectors also express a stronger interest in art investment funds (50% this year, up from 29% in 2021). Younger demographic (below age 35), where 66% (50% in 2021) said socially responsible investment products in culture would appeal the most to them.

Porsche welcomed its Chinese audience into the group’s Web3 community this week with its “911-Dreamer” digital collectibles drop. Photo: WeChat

How is technology, especially blockchain and digital art, influencing the art and finance industry?

Technological innovation drives the art and finance sectors closer together. Most of the advancements seen in the intersection between art and technology are also going to benefit the future development of the art and finance industry. 64% of wealth managers surveyed this year said that technology could be a catalyst for incorporating art and collectible assets into their existing wealth management services. While only 18% of wealth managers in 2019 said that blockchain technology could have a significant impact on the development of art and wealth management services, a significantly higher proportion (58%) of wealth managers said the same this year.

Blockchain technology as a register for art and collectibles. This year, 58% of wealth managers said that blockchain technology aimed at creating a registry and provenance tracking tool for art and collectibles could have the most impact on art and wealth management services in the future

Blockchain technology as a Decentralized Finance (DeFi) tool. 43% of wealth managers believe that blockchain technology as a DeFi tool would allow better integration of art and collectibles into wealth management through tokenization

- Increased access: Web3 technologies could enable tokenization and fractional ownership of artworks and collectible assets, allowing multiple investors to own a share of a single artwork. This can democratize the art market and allow a wider range of investors to participate in art investment.

- Risk reduction: By sharing the ownership of an artwork, investors could reduce their risk exposure to a single asset. This could help to mitigate the risk of loss due to market fluctuations or damage to the artwork, for example.

- Increase liquidity: Fractional ownership could potentially increase liquidity in the art market by allowing investors to buy and sell shares in an artwork more easily than they would be able to with a standalone artwork. This can increase the flexibility and efficiency of art investment.

- Expanded investor base: Fractional ownership could attract new investors who may not have previously considered investing in art due to the high costs involved. This could, in turn, increase

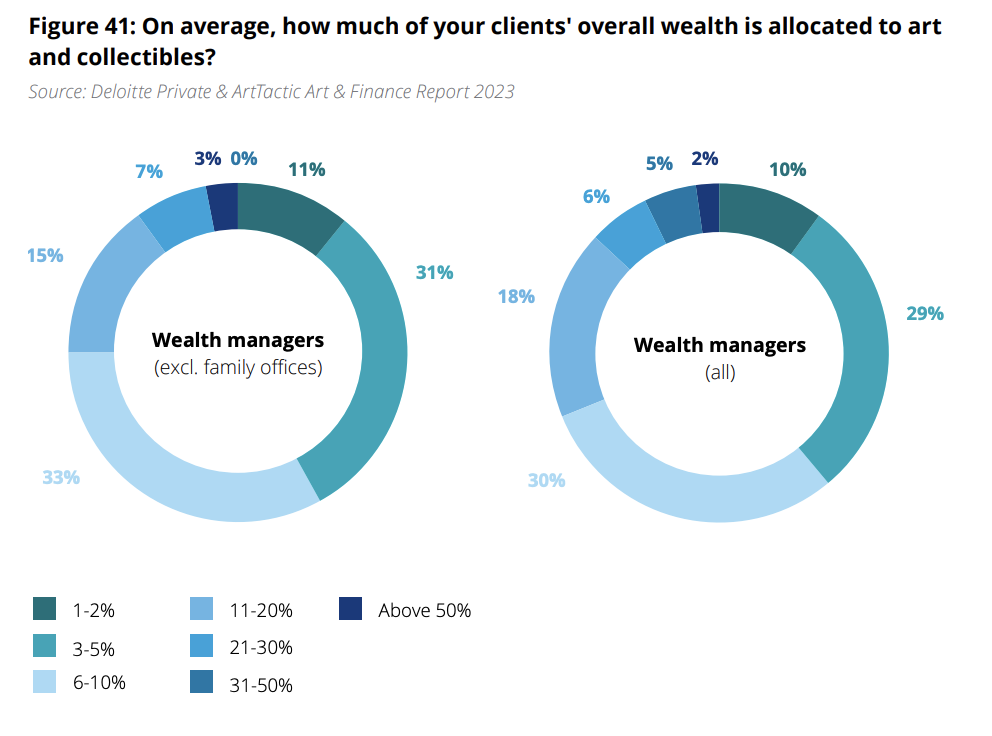

What challenges do wealth managers face in integrating art into their broader wealth management offerings?

Despite some improvements in recent years, the challenges of integrating art into wealth management remain. The lack of regulation and transparency still dominates, but the number of wealth managers identifying these as key obstacles has decreased since 2017. This suggests that recent developments around anti-money laundering (AML) regulation, as well as technology’s role in increasing transparency, are starting to change wealth managers’ perceptions of these challenges.

Four out of 10 wealth managers said that lack of internal interest and leadership continues to be an issue. This could be due to a lack of understanding of the benefits considering that 44% of wealth managers said demonstrating the cost-benefit of including art in wealth management was a key challenge, and 42% said lack of internal expertise remains an obstacle.

Image: Deloitte

Based on current data, what future trends can we anticipate in the intersection of art, collectibles, and wealth management?

After 12 years and eight reports:

- Fine art and collectibles are unique assets with specific attributes that elicit and cover a range of motivations. This special asset class offers great opportunities for wealth managers to connect with their clients and create a unique relationship based on emotion and purpose, but also on financial considerations.

- Fine art and collectibles assets are normally poorly addressed, despite representing a sizeable portion of HNWIs’, and in particular HNWIs collectors’, wealth. However, in a holistic wealth management service offering, there is a fiduciary responsibility to address this through services that cover wealth protection, monetization, wealth transfer and also investment.

- Several trends are slowly, but surely, driving family offices and wealth managers servicing UHNWIs to consider how to incorporate clients’ collections and passions into their service offerings for UHNWIs. These include technological developments, increased awareness of the role of art and collectibles in wealth management, increasing competition in the wealth management sector —coupled with client demand and increasing interest for alternative investments.

- We see positive signs for the future potential of the art and finance industry. The need to modernize existing business practices to increase trust and transparency in the art market is recognized. Adaptations needed to respond to the expectations of a new generation of collectors are visible to wealth managers. Increased emphasis on purpose and social impact investment and growing recognition of the role that culture plays in society could create new opportunities. And the expansion of art and finance to include luxury assets, and even the development of fractional ownership, may evolve how we conceive of this dynamic industry.

How have recent geopolitical events influenced the global art market, particularly in emerging economies?

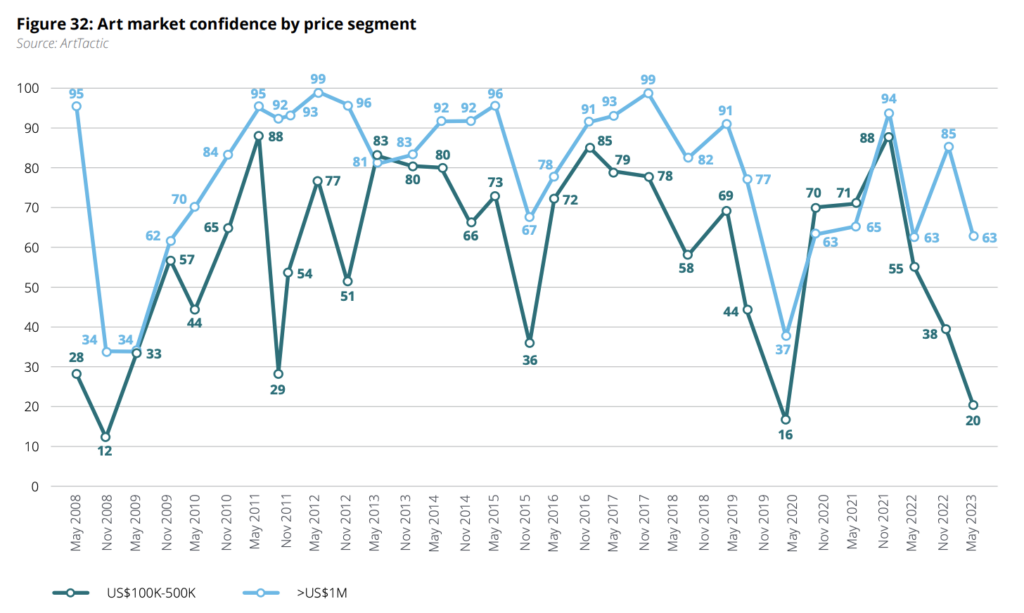

Art market confidence deteriorates in the face of continued economic uncertainty. Higher inflation, rising interest rates and stagnant growth continue to weigh negatively on the economic component of the ArtTactic Art Market Confidence Indicator. However, while still in a deeply pessimistic territory, the economic indicator has risen from 18 in February 2023 to 23 in July 2023, with more respondents believing the economic situation could stabilize this year.

The art market slowed down in the first half of 2023 as high-end supply dried up. Overall auction sales at Christie’s, Sotheby’s and Phillips were down 18.2% year-on-year in the first half of 2023, with fine art sales plummeting by 31%. The drop in global fine art auction sales has been largely driven by a much lower supply of trophy lots; only 40 lots sold above US$10 million in the first six months of 2023, generating a combined total of US$932 million, compared to 75 lots in the first half of 2022, with a total sales value of US$2.06 billion. The downturn has had a different impact on different regions.

Although Hong Kong auction sales were down in 2023, this market held up better than New York and London. Overall, Hong Kong Marquee evening sales this year (Spring and Autumn) were down 7% compared to 2022. This compares to a year-on-year decline in New York’s Marquee evening sales of 36% and a 24% fall in sales for London Marquee evening sales in 2023, suggesting that the Asian market has been more resilient than the other major market regarding the very top end of the art market.

A neutral-to-negative 12-month art market outlook could mean that the market is settling at lower levels 59% of art market experts surveyed believe the art market will remain flat over the next 12 months, and sales will settle at lower levels already seen in the first six months of the year. However, 28% believe there will be further downside in the art market over the coming year, while 13% believe the market has reached its bottom and will recover in the coming months.

Confidence is deteriorating across all price segments. ArtTactic’s confidence indicators have weakened across all price segments since February 2023, with particularly low levels of confidence in the mid-market segment, or artworks priced in the US$100,000– US$500,000 range. Although the majority of respondents remain positive about the US$1 million-plus segment, the indicator has fallen 26% since February 2023, which means even the top end of the art market is feeling the uncertainty. This is already evident in the lower levels of supply of US$1 million artworks in the first half of 2023.

Image: Deloitte

Is there an increasing trend towards sustainable and socially responsible investments in the art world, and how is this shaping the market?

Social impact investment and sustainability in the arts and culture sector exist at the intersection between philanthropy and investment. It is a relatively new area for the art wealth management industry. It provides wealth managers with a new client service that focuses on social impact and purpose-led investment in the arts and culture sector.

Sustainable impact investment in art and culture could become an attractive investment model, especially for the younger generation. In this year’s survey, we have seen a slight increase in interest in arts and culture-related sustainable impact investment among art professionals, wealth managers and NextGen collectors. 24% of collectors (28% in 2021), 30% of art professionals (23% in 2021) and 30% of wealth managers (21% in 2021) identified sustainable impact investment in the arts as the most attractive investment model.

This was significantly higher among the younger demographic (below age 35), where 66% (50% in 2021) said socially responsible investment products in culture would appeal the most to them. This implies that wealth managers who expand their sustainable investment offerings are well-positioned to attract and engage the younger client segment in the future. This suggests that broader investment trends, such as increasing focus on ESG-compliant investments, could also be filtering down to the cultural space.